This website will be decommissioned shortly. To visit the new AORA Law website please follow this link.

The Opportunity

UK Real Estate Investment Trusts (REITs) are tax-efficient property investment vehicles. No corporation tax is paid on the profits of a REIT’s UK property rental business. Instead, the tax charge is pushed back to the investors as though they had invested directly in the property themselves. REITs, therefore, combine the tax benefits of a direct property investment with the economies of scale that come with investing through a fund.

To become a REIT, a company must meet several technical conditions.

AORA’s tool

AORA’s REIT tool covers all the tests a company needs to meet to enter this desirable regime.

Its speed and efficiency allow practitioners to design REIT structures with ease. Data inputs can quickly and conveniently be changed to produce alternative scenarios for comparison. Potential grey areas and speculative positions are eliminated from the analysis, making the exploration of options and the optimisation of a client’s tax position significantly easier. The resultant effect on the quality of service offered is profound.

Our reports are ready for review and strategic input by senior practitioners. Their comprehensive footnoting makes them an ideal learning tool for junior practitioners finding their way around this complex area of law for the first time.

You can see example reports generated by AORA’s REIT tool below.

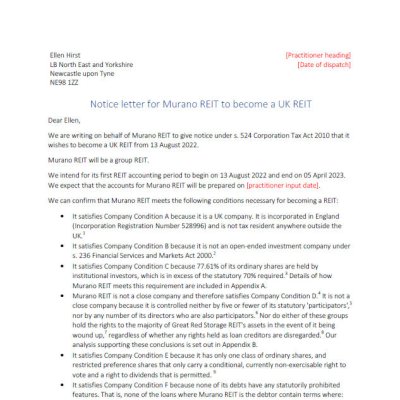

Complex Case Success Letter HMRC

Complex Case Success Letter HMRC

Example output of a letter to HMRC confirming eligibility for a client to become a UK REIT. Simple Case Fail Letter HMRC

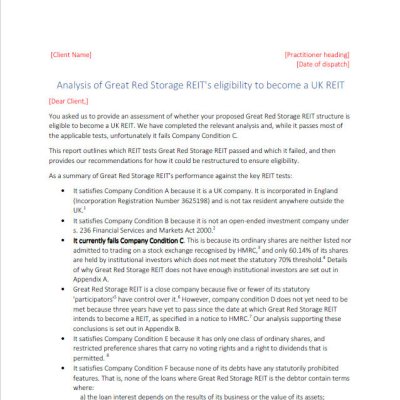

Simple Case Fail Letter HMRC

Example of letter output for a case which fails to meet the requirements to become a UK REIT. Simple Case Success Letter HMRC

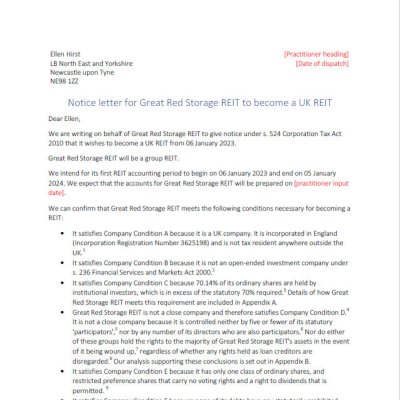

Simple Case Success Letter HMRC

Example of ouput letter for simple case which meets the criteria for becoming a UK REIT.